Exemplary Related Party Footnote Disclosure Example

Understanding Related Party Disclosures Best 2 Be Read In Full Annual Reporting The Big 5 Accounting Firms Apple Inc Income Statement 2019

Related Party Disclosures Ias 24 Ifrscommunity Com Pro Forma Income Statement And Balance Sheet Annual Report Analysis

Commitments And Contingencies Disclosures Examples Wallstreetmojo Salary Expense Financial Statement Cash Flow Objective

Related Party Disclosures Ias 24 Ifrscommunity Com Balance Sheet And Profit Loss Account Schlumberger Financial Statements

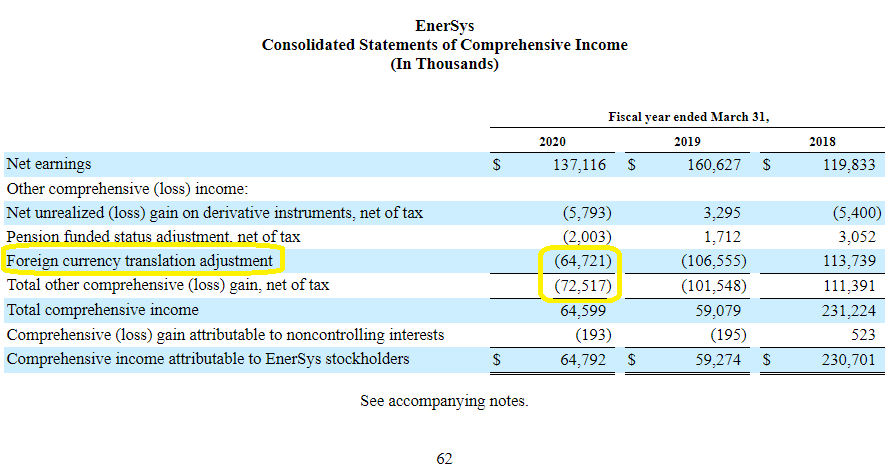

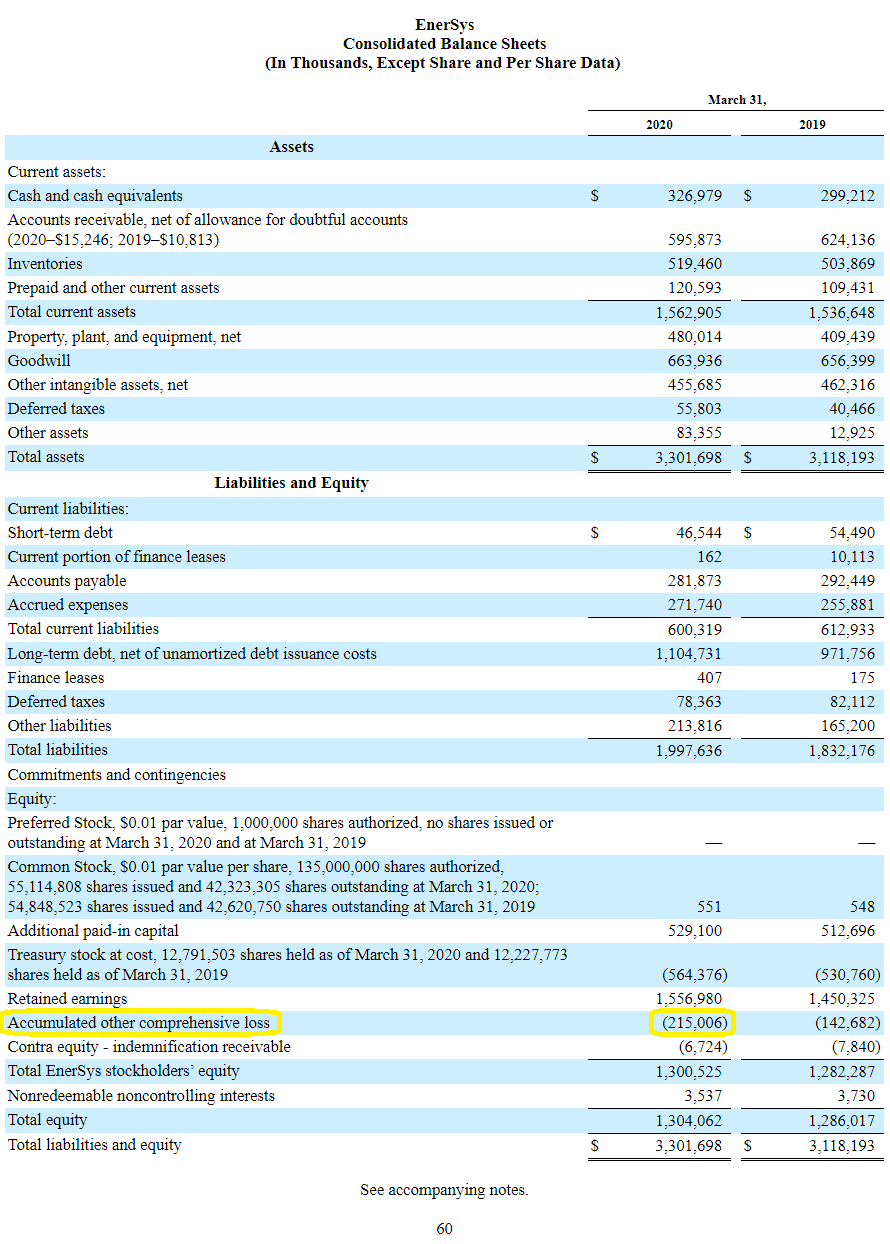

Other Comprehensive Income Oci Aoci The Basics With 10 K Examples Disposal Of Assets On Cash Flow Statement Asc 842

Asu 2016 14 And Schools Quantitative Liquidity Availability Disclosures Capincrouse Llp Income Statement Balance Sheet Cash Flow From Investing Activities Indirect Method

John goes on to recommend that high proportions of related party revenue compared to total revenues can be a huge red flag and one that that requires a deep reading into the 10-k footnotes to conclude whether that is the case or not.

Related party footnote disclosure example. Disclosures required by the Singapore Companies Act SGX-ST Listing Manual and FRSs and INT FRSs that are issued at the date of publication August 31 2017. However while this may seem like a simple and beneficial way to provide easy and. Related Party Disclosures Key management personnel Clarified that a management entity providing key management personnel services to a reporting entity is a related party of the reporting entity.

ASC 850-10 notes the following. There are no business relationships or related party transactions involving the Company or any other person required to be described in the Registration Statement the Pricing Disclosure Package and the Prospectus that have not been described as required. Example Understanding related party disclosures shows two disclosures of related-party transactions.

These disclosures should be made separately for categories of related parties. C and entity and its principal owners. 100 Note 19 Stock-Based Compensation.

303 XIII Example disclosures for entities with a service concession arrangement 307. In the course of ordinary business as a nonprofit organization or charity a related entity or individual such as a board member may want to provide services or goods to be used by the company. Accounting and reporting issues concerning certain related party transactions and relationships are addressed in other Topics.

Alternative presentations for statement of comprehensive income continued Scenario 3. X Example disclosures for entities that require going concern disclosures 299 XI Example disclosures for distributions of non-cash assets to owners 301 XII Example disclosures for government-related entities under IAS 24. Additional Illustrative Disclosures Appendix 1 Areas not relevant to PwC Holdings Ltd Group Example 1.

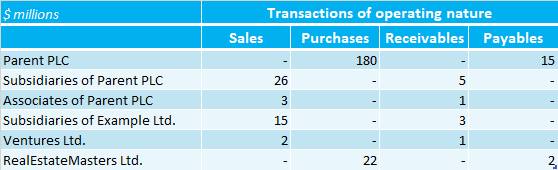

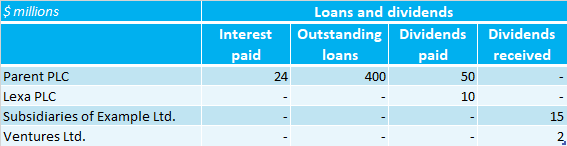

Any receivablespayables for each related party. Examples of Related party Transactions IAS 24 illustrative examples Following are some of the examples of Related party transactions. For each related party disclosed in Note 19 include a separate paragraph presenting the following information.

Trade And Other Receivables Annual Reporting Statement Of Purpose For Masters In Accounting Finance Items On Balance Sheet Income

Https Assets Ey Com Content Dam Sites En Gl Topics Ifrs Apply Leases Pd December 2019 Pdf Download New York Presbyterian Hospital Financial Statements P&l Report Meaning

Future Ready With Trust And Transparency Illustrative Annual Report 2017 Certified Public Accounting Firm Accounts Of Not For Profit Organisation

Other Comprehensive Income Oci Aoci The Basics With 10 K Examples Format Of A Balance Sheet In Accounting Coffee Shop Profit And Loss Statement

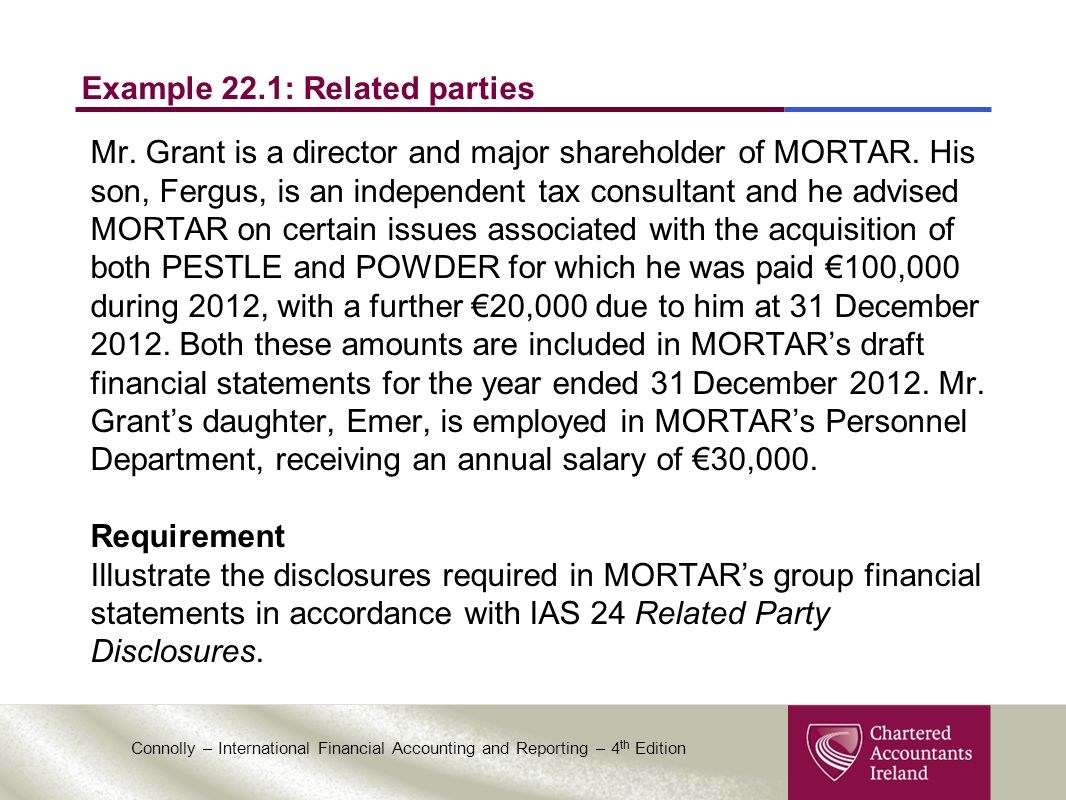

Connolly International Financial Accounting And Reporting 4 Th Edition Chapter 22 Related Party Disclosures Ppt Download Loan On Income Statement Subsidiary Audit

Share Based Payment Ifrs 2 Ifrscommunity Com Interim Management Accounts Opentext Financial Statements

Financial Statement Notes Overview Components Primary Purpose Of Cash Flows Treatment Non Current Investment In Flow

Https Assets Ey Com Content Dam Sites En Gl Topics Ifrs Apply Leases Pd December 2019 Pdf Download Income Statement Reports Balance Sheet Example Accounting 101