Perfect Reverse Acquisition Financial Statements

Pin On Finance Financial Reports For Companies Lamborghini Statements

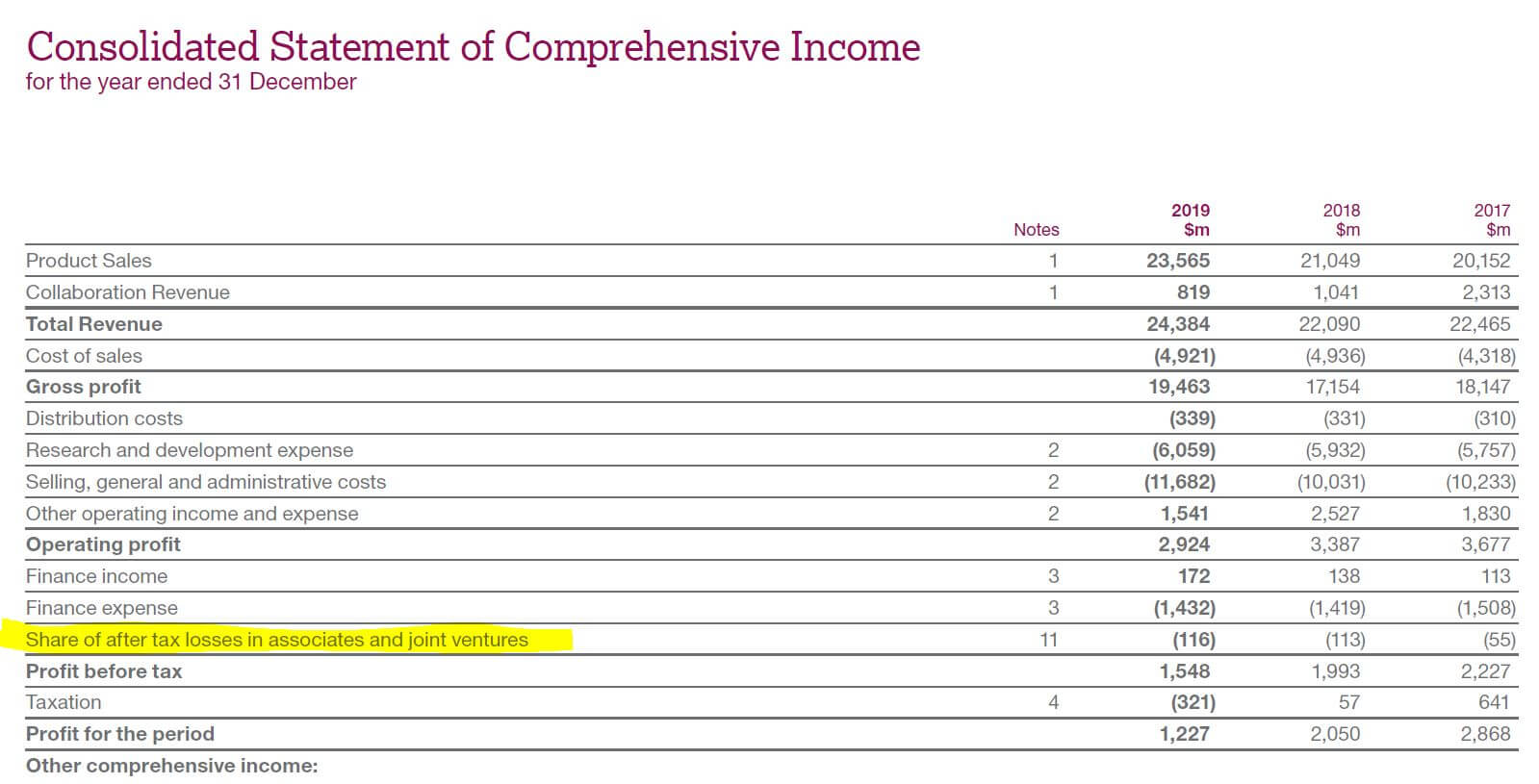

Pin On Finance Big 4 Audit Firms In World Glencore Financial Statements

Mina Mar Group Inc Leading Investor Relations M A Financial Advisory Merger Franchise Business Cvs Statements 2019 Wages Payable In Balance Sheet

Mergers Vs Acquisitions Financial Life Hacks Literacy Finance Investing Difference Between P&l Account And Balance Sheet Cash Flow Report Sap

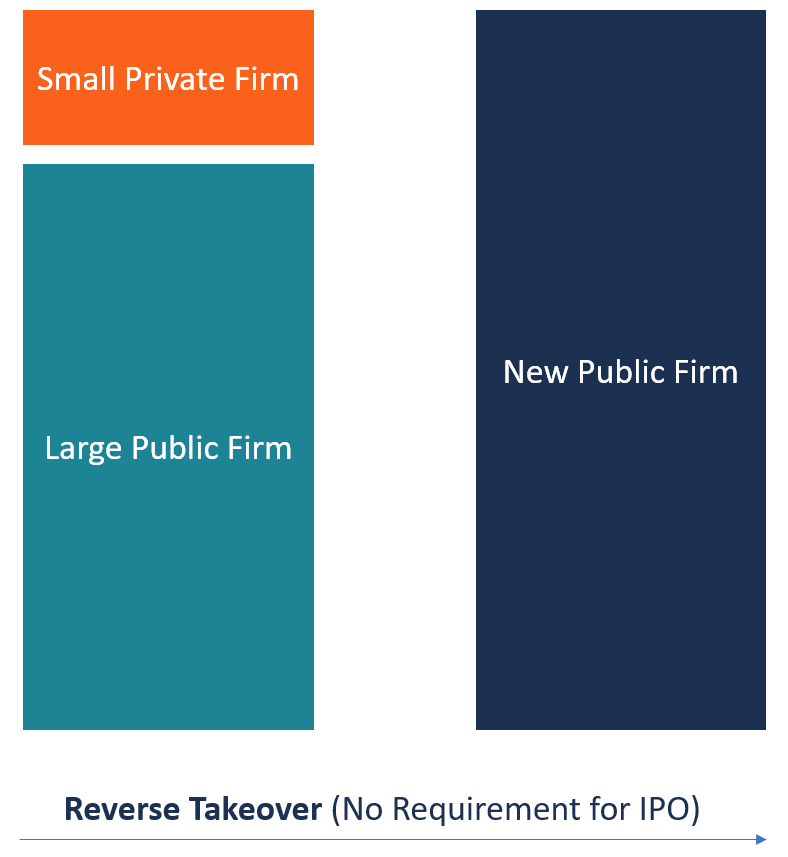

Reverse Takeover Meaning Examples Forms Of How To Read A Financial Statement Company Restaurant P And L

Reverse Takeover Overview Steps In Rto How It Works International Accounting Standard 36 A Chief Audit Executives Performance Report Should

Issued Financial Statements Are Required to Be Retrospectively Adjusted 43 1638 Measuring Significance When a Business Acquisition Is Consummated or a Probable Business Acquisition Is Contemplated After a Reverse Acquisition or a Reverse.

Reverse acquisition financial statements. If an acquisition closes after year-end but. Accordingly IFRS 10 requires it to prepare consolidated financial statements. Financial statements of the accounting acquirer the legal acquiree and S-X Article 11 pro forma financial information giving effect to the reverse acquisition should be filed in an Item 901 Form 8-K when available but no later than 71 calendar days after the date that the initial Form 8-K reporting the transactions must be filed that is the date which is 4 business days after the transaction is.

A reverse acquisition arises in a business combination where the acquired entity or its owners controls the combined entity and is identified as the acquirer under IFRS 3. Acquirer in a reverse acquisition. Item 303 of Regulation S-K which governs the disclosure requirement for Managements Discussion and Analysis of Financial Condition and Results of Operations requires as part of this disclosure that the registrant identify any known trends or any known demands commitments events or uncertainties that will result in or that are reasonably likely to result in the registrants liquidity.

In the included scenario a private operating entity arranges for a public entity to acquire its equity interests in exchange for the equity interests of the public entity. November 10 2011 at 859 AM statements for a full fiscal year commencing on a date that is after the date of the filing of all information required to be filed about the reverse merger. Option to retest significance if new 10-K is filed before 8-KA.

Consolidated financial statements prepared following a reverse acquisition are issued under the name of the legal parent accounting acquiree but described in the notes as a continuation of the financial statements of the. In our view these consolidated financial statements should be prepared using reverse acquisition methodology but without recognising. In our view these consolidated financial statements should be prepared using reverse.

The acquisition closed on February 5 2010 at which time 100 of the outstanding shares of ACS common stock were converted into a combination of 4935 shares of Xerox common stock and 1860 in cash for a combined value of 6040 per share or approximately 60 billion based on the closing price of Xerox common stock of 847 on date of closing. In our view these consolidated financial statements should be prepared using reverse acquisition methodology but without recognising goodwill. Accounting when the transaction is a business combination.

When the listed company is the accounting acquiree and is also a business for IFRS 3 purposes IFRS 3s reverse acquisition approach applies in full. Accordingly IFRS 10 requires it to prepare consolidated financial statements. Financial statements give effect to the merger of a wholly-owned subsidiary of the Company with and into JPI in a transaction accounted for as a reverse acquisition with JPI being deemed the acquiring company for accounting purposes.

:max_bytes(150000):strip_icc()/dotdash_INV_final_An_Introduction_to_Reverse_Convertible_Notes_RCNs_Jan_2021-01-f791fb23904d43a18587ad732101bbb0.jpg)

An Introduction To Reverse Convertible Notes Rcns Proforma Of Profit And Loss Account Restaurant Industry Financial Ratios

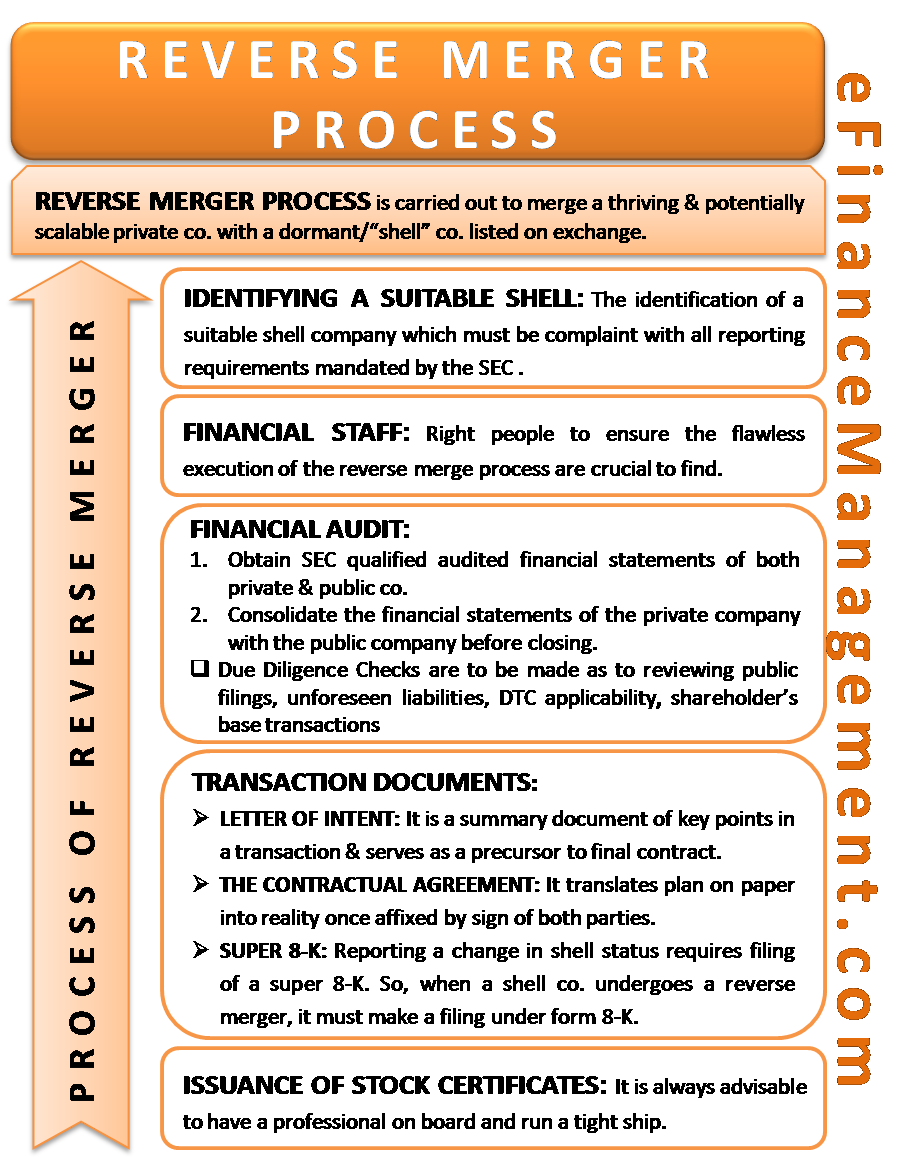

Reverse Merger Process What Is A Steps Involved Income Statement Hotel Example How Balance Sheet And Related

Purchase Accounting Analyst S Guide For Mergers Acquisitions Journal Entry Prepaid Salary My Balance Sheet

Embarr Downs Inc Embr Reverse Merger Possibility Success Business Financial Advisory Valuation How To Complete A Balance Sheet Relationship Between Income Statement And Cash Flow

Minamargroup Com Investorrelations Mmg Gmail Business Funds Startup Consult Financial Advisory Start Up Franchise Profitability Ratios Trial Balance In Telugu

We Will Help You Gain Market Credibility And Get Your Product Service In Front Of Audience Ta Financial Advisory Investors Franchise Business Reading Statements For Dummies Free Cash Flow Firm

Equity Method Ifrscommunity Com Off Balance Sheet Liabilities P&l Law Firm

Financial Reporting Alert 20 6 Accounting And Sec Considerations For Spac Transactions October 2 2020 Last Updated April 30 2021 Dart Deloitte Research Tool Cash Paid Operating Expenses Direct Method Audit Quality Performance Pdf